TCJA Amortization Rule - Will it Stick?

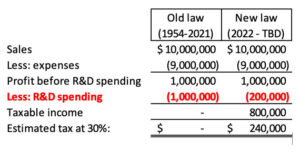

For decades, Congress has recognized that companies engaging in research shouldn’t be penalized. Since 1954, businesses have been able to write off R&D expenses in the year they incur them, without having to amortize the spending over time. Yet in 2017, the Tax Cuts and Jobs Act (“TCJA”) put this in jeopardy by including a provision that would eliminate the immediate expensing of R&D costs starting in 2022.

If left unchanged, domestic R&D spending would be amortized over 5 years and foreign R&D spending would be amortized over 15 years. Now that it’s 2022, what are the impacts?

Many R&D experts are optimistic this new regulation won’t stick. When the TCJA was passed, the change to R&D expensing was generally viewed as a maneuver to balance the budget, with the hope that a future Congress would be able to delay or undo this change.

Progress has already been made: the 2021 Build Back Better Act included a provision that would delay the TCJA amortization rule until 2026. Although this act did not become law, it shows that Congress is willing to delay the effective date. Congress recently tried again while passing the CHIPS Act.

For now, we’ll have to wait and see what happens.